With the election less than two weeks away we turn to scenario planning for the market impact of the potential outcomes from the vote. While a Conservative majority is the most likely outcome at this stage, we know, to paraphrase Harold Wilson, that one week is a long time in politics, let alone two.

We have reviewed opinion poll data, betting markets and calculations on the likely outcome in terms of seats in Parliament from sites such as this electoralcalculus.co.uk

Our conclusions are that while Boris Johnson is currently looking likely to still be Prime Minister on December 13th, and is odds-on to have a Parliamentary majority, probability weighting the outcomes seems to explain why UK equities, gilts and sterling are trending sideways so far during the campaign. That looks rational.

There are also rational reasons to think Labour’s poll ratings could rise from here as we detail below. In our view market volatility will likely return when we know the election result.

- Most likely outcome

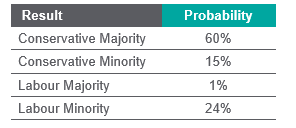

Let’s jump straight to our conclusion which is summarised in this table:

The probability of Boris Johnson being Prime Minister is 75%. But clearly the market impact of a majority Conservative government is likely to be different to that of a minority Conservative government.

Jeremy Corbyn has a 25% probability of being Prime Minister but a de minimis chance of having a working majority. Again, the market impact of each scenario that puts the Labour leader in 10 Downing Street is rather different.

2. Market impact of each outcome and why markets have been directionless so far in the campaign

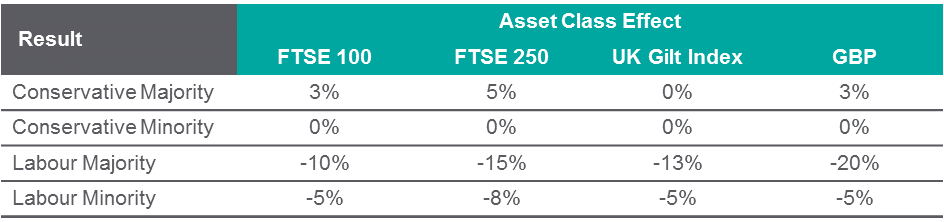

Here we have looked at market moves in recent months and in 2017 to give our best guess on the reaction to each outcome in the first month after the election. This is very much an art, not a science. But we hope this at least gives a sense of the likely direction of travel in the days immediately after the election.

Whatever your own political views, we think it reasonable to say that the best outcome for markets will be a Conservative majority while the worst would be a Labour majority.

We have not suggested that a Conservative majority will lead to a roaring bull market because in our view there remain a lot of challenges to overcome that will keep an “uncertainty discount” on UK assets, but a much reduced one from that which has afflicted the country for much of the last three and half years.

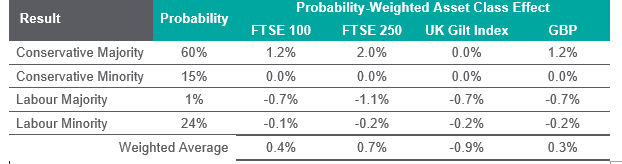

If we put our probabilities together with our asset class effect assumptions we can produce the below Probability Weighted Asset Class Effect.

This table could give us a reason why markets have been so calm and non-directional in the campaign so far. If the above is right then the election will have some effect when we know the result but before then it does not make much sense to take a big position one way or the other.

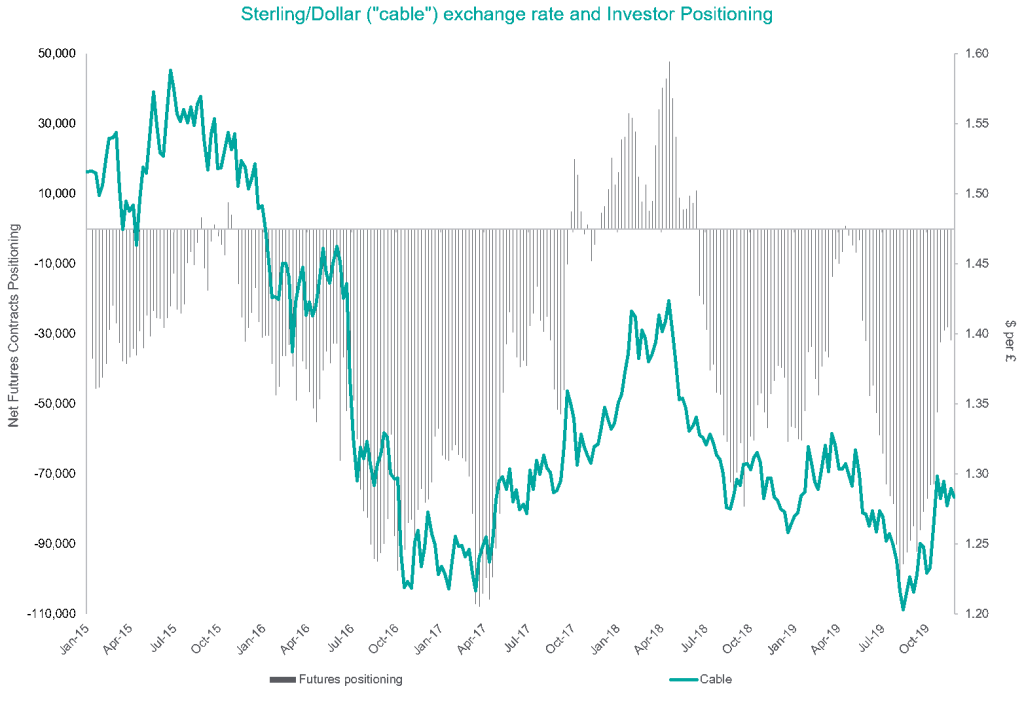

That is reflected in the data on positioning in the currency markets, much the most liquid way to trade a view on UK macro risk. As the chart below shows, investors have reduced sterling short positions since they peaked in early August but since the start of the election campaign positioning has been stable at a smaller net-short than in August. That seems entirely rational given the analysis above.

3. Opinion Polling data so far and how things could change in coming days

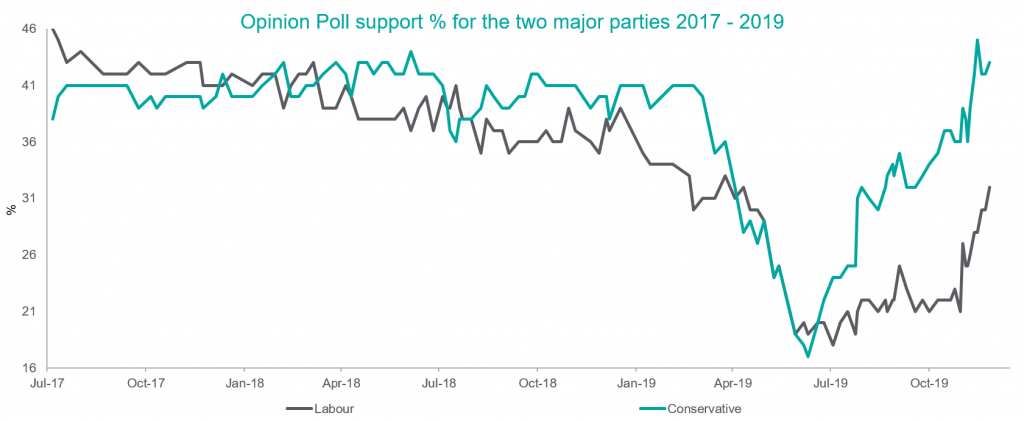

The Conservative vote has reached levels not seen since 2017 in current polls (green line above). It is possible that we are at “peak Tory” share of the vote so the more interesting question is will the Labour vote (black line) continue its own ascent?

One way of thinking about this is to track the vote share of the two major parties. One of the remarkable things in a year when on several days we seemed to see six impossible things before breakfast, was the collapse in the support for each of the major parties earlier this year. This coincides with the failure to leave the European Union on March 29th which those of you with long memories will remember was the first irrevocable deadline for us to miss.

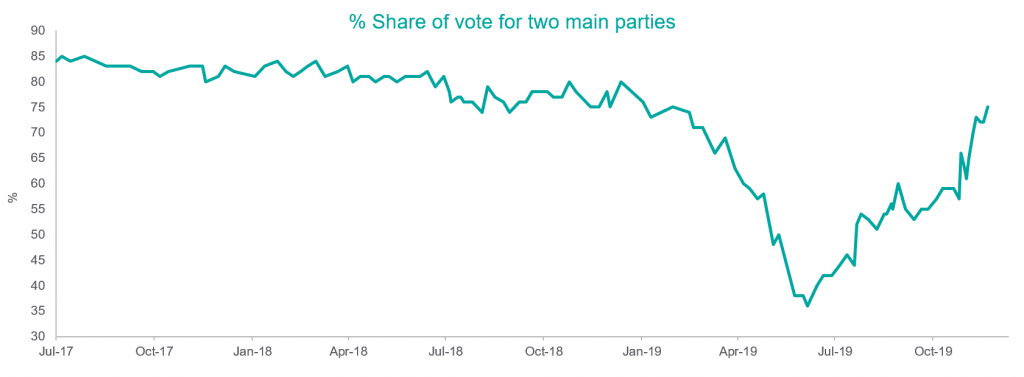

As the chart below shows, the share of the two parties is now back to 75%. Having begun to recover over the summer, it has continued to recover in the campaign.

To digress for a moment, one by-product of this is that in a first-past-the-post electoral system, modelling the translation of vote share into seats won is much easier when there are two dominant parties. At the beginning of the campaign, when the two major parties were at a combined 59%, we were rather suspicious of such models. Today we think we can have more confidence in them. Most continue to suggest a Conservative majority.

For example, the widely anticipated, because it was the most accurate in 2017, YouGov MRP survey was released on 27th November. It is a detailed constituency by constituency survey involving interviewing 10,000 respondents and then regressing the data. It shows a Conservative majority of 68 seats.

So far the rise of the two main parties has been due to the squeeze on the Brexit party by the Conservatives and the squeeze on the Liberal Democrats from Labour. As discussed above, the Conservatives have probably squeezed the Brexit Party as far as they can so the question is whether Labour can continue to increase its share at the expense of the Liberal Democrats. If Labour can, then the race could narrow.

One way this could happen is if the issues dominating the campaign shift. We said in our October 30th report that we thought the Conservatives would win the election if the campaign was dominated by Brexit. So far that has been the case.

YouGov’s latest polling says that “Britain leaving the European Union” remains the single most important issue in the campaign with 66% of voters including it in the three issues they think are the most important. It has remained the most important issue since the 2016 referendum when this question has been asked by YouGov.

The Conservative Party have become the party of Brexit and as long as it is the most important issue that is good for the chances of a Conservative majority.

Brexit is one “Tory issue” but there are others. Traditionally the issues that the Conservatives tend to poll well, in the sense of being trusted by the electorate to do a good job on, include things like crime and the economy. It has also been the case in recent years that immigration has become more important and those for whom it is are more likely to be Tory voters (if not UKIP or Brexit).

For Labour, the issues that it tends to poll well on are health care, education, the environment and housing. One of the reasons that many Labour voters were pro-Brexit is that there are plenty of reasons for voters to be genuinely concerned about these issues. When given the chance to express a view in the EU referendum the concern and disillusionment about many of these issues contributed to the Leave vote (as of course did concerns about immigration).

One way to think about whether the issues that are the most important in the campaign are favourable to one party or the other is to take the three most frequently mentioned issues that fit into those “traditional” Tory and Labour blocs. The chart below shows the result.

The chart adds together the % of voters mentioning Brexit, Immigration and the Economy and showing those as the green “Tory issues” line. It adds up to over 100% as voters can mention three issues.

The black line shows the proportion of voters mentioning health, education and the environment as the most important issues.

There is good news for Labour in this chart. The focus on those “Labour issues” has been picking up this year and if that continues it will almost certainly mean that the Labour share of the national vote in opinion polls will continue to rise. Put simply, can Labour keep the focus on the NHS?

4. Betting Markets

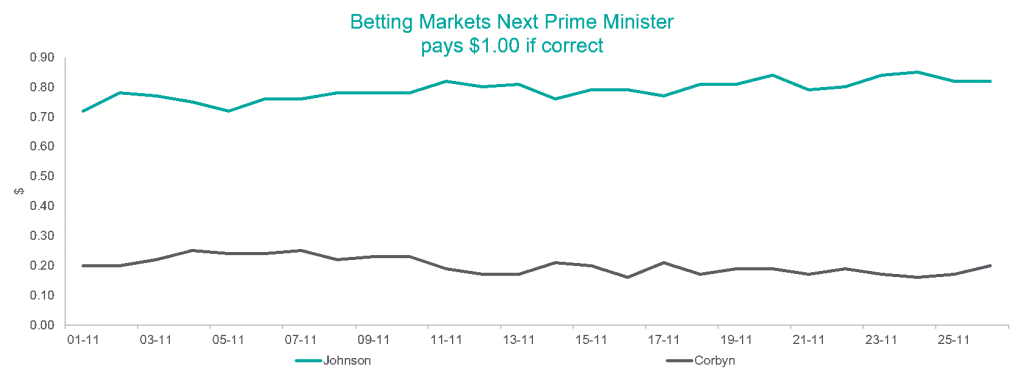

Although betting markets, like the polls, were unreliable in 2017 and in the referendum, they still provide information that helps either confirm or question the message from the polls and from markets. So far they are consistent with both.

Below is the view from one betting market, predictit.org. There has been a slight drifting up in the probability of Johnson being PM (although this says nothing about the probability of his having a majority). We are taking a more prudent view than the betting markets on the respective probabilities of each candidate for PM but there is no new material information in this dataflow at the moment.

Conclusion

Market reaction to the election uncertainty has been completely rational in the campaign so far. A probability weighted distribution would suggest that UK markets will drift sideways until the election itself at which point volatility will increase.

At the moment, all the information available points to a Conservative majority. But there is hope for Labour in the way it has squeezed the Liberal Democrat vote and in the way the electorate is reporting what issues it is most concerned about.

We will do another update on our thinking before election day. But for now, we believe there is all to play for.

William Dinning

29th November 2019

Risk Warnings

The views and opinions expressed are the views of Waverton Investment Management Limited and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All material(s) have been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy of, nor liability for, decisions based on such information. Changes in rates of exchange may have an adverse effect on the value, price or income of an investment. Simulated performance is no guarantee of future results and the value of such investments and their strategies may fall as well as rise. Capital security is not guaranteed.