Throughout March, the war in Ukraine continued to dominate headlines and affect investment portfolios around the world.

Many companies, from well-known businesses like L’Oréal and Coca-Cola to smaller firms, have withdrawn operations from Russia, including online sales. Others, such as Unilever and Nestlé, have halted investment in the country but are continuing to provide some goods.

This has led to some volatility within the markets, although they did rally towards the end of the month.

Sanctions on Russia mean the price of some goods have boomed globally. Aluminium reached a record high, and the price of fuel also climbed. As both Russia and Ukraine are major exporters of wheat and corn, the conflict may affect food prices too.

The ongoing uncertainty has played a role in the higher levels of inflation many countries are experiencing. The after-effects of the pandemic and the supply issues it caused are also partly to blame for inflation rates.

It’s natural to be worried about your plans during times of uncertainty. What’s important is that you keep your long-term plans in mind and don’t make knee-jerk decisions based on headlines. If you have any questions about your investment strategy or wider financial plan, please contact us.

UK

Chancellor Rishi Sunak delivered the spring statement on Wednesday 23 March.

He opened with subdued growth forecasts from the Office for Budget Responsibility (OBR). The organisation now expects GDP to rise by 3.8% in 2022, down from the 6% forecast in October last year.

Among the measures Sunak announced were a fuel duty cut of 5p a litre as prices at petrol stations soared, and a cut in VAT for home energy efficiency installations.

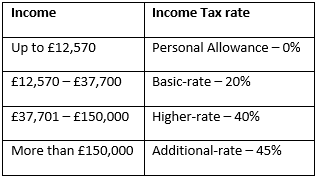

While the government will continue with its plans to raise National Insurance (NI) in the 2022/23 tax year, the threshold that workers will start paying NI will increase.

The National Insurance Primary Threshold and Lower Profits Limit will rise from £9,880 to £12,570 from July 2022. Sunak also suggested that the basic rate of Income Tax could be cut in 2024, but only if certain conditions were met.

The statement followed the news from the Office for National Statistics (ONS) that in the 12 months to February 2022, inflation reached a 30-year high of 6.2%. The rate is now expected to peak at around 8%, but the Bank of England (BoE) hasn’t ruled out the possibility of double-digit inflation.

In a bid to slow the pace of inflation, the BoE also announced a base interest rate rise. It’s the third time the BoE has increased the rate since December 2021, and it now stands at 0.75%.

Inflation rising means that, in real terms, basic pay fell by 1% in the year to February – the steepest decline since 2014 – according to the ONS.

One of the biggest challenges families are facing is the rising cost of living, particularly energy prices. British wholesale gas for April delivery has increased by 20%. If prices remain high it could mean that household energy bills, which will be rising on average by 54% in April, will rise even further following the next review in October.

It’s an issue that is also affecting businesses. The Confederation of British Industry (CBI) has urged the government to offer support as energy bills rise. A CBI survey found that this pressure could lead to rising prices. 82% of British manufacturers expect to increase prices in the coming months.

As consumers are forced to cut back, some businesses are likely to find they’re affected by a reduction in discretionary spending.

Another news story that caught the attention of headlines was P&O Ferries’ decision to dismiss 800 members of staff and replace them with agency workers, who would earn less than the UK minimum wage. The decision caused outrage, prompted safety concerns, and led to suggestions that it may have been illegal.

Europe

Much like the UK, European economies are struggling with inflation and rising energy costs.

The European Central Bank (ECB) has raised its inflation forecast for 2022 to 5.8% compared to its earlier prediction of 3.2%. Again, energy prices are having a significant effect as costs increased by more than 30%.

Christine Lagarde, the president of the ECB, said the war in Ukraine “will have a material impact on economic activity through higher energy and commodity prices, the disruption of international commerce, and weaker confidence”.

However, unlike the BoE, the ECB elected to hold its interest rate at 0%.

The war in Ukraine has affected the outlook of Europe’s largest economy, Germany. A report from the Ifo research institute reported that business confidence in the economy has “collapsed” since the start of the conflict due to energy and supply chain challenges.

An agreed partnership between the European Commission and the US to reduce Europe’s reliance on Russian energy could relieve some of the pressure later this year. The US will aim to deliver larger shipments of liquefied natural gas to cut the European Union’s dependency on Russian Gas by two-thirds this year and end it before 2030.

After limiting activity for a month, the Moscow stock exchange reopened on Monday 28 March. Unsurprisingly, stocks fell but measures were put in place to prevent a sharp sell-off, including banning foreigners from selling Russian shares.

US

Inflation in the US increased to 7.9% in the 12 months to February 2022 – a 40-year high – according to the Labor Department.

The rising cost of living is having a knock-on effect on consumer confidence. A barometer from the University of Michigan found falling incomes in real terms means consumer sentiment has fallen to an 11-year low.

Despite the challenges, employment statistics indicate that businesses remain confident. The unemployment rate fell to 3.8% after firms took on 678,000 workers, far higher than the 400,000 expected, according to the Bureau of Labor Statistics.

US technology companies Alphabet (Google) and Meta (Facebook) are facing an antitrust investigation launched by the EU and UK. The two firms are accused of colluding to carve up the online advertising market between them. The deal between the two firms is already under investigation in the US. If found to be illegal, the deal, called “Jedi Blue”, could result in hefty fines of up to 10% of their global turnover.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only. The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.